Federal Reserve Series: What is WRESBAL?

Federal Reserve Series: What is WRESBAL?

This article explains the main liquidity variable frequently used in some of the Darkly Energized TradingView indicators and charts.

Much of the data I use in my charts comes straight from the Federal Reserve. In this post I want to help readers make sense of a very popular liquidity series called WRESBAL, which is updated on FRED’s site each Thursday (with Wednesday values) after market close.

This is a chart of WRESBAL going back prior to the start of QE in 2008:

By looking at this, one can see how the balance was effectively 0 or close to nothing until QE started, and with this balance came an acceleration in asset valuations.

Cracking the WRESBAL Code

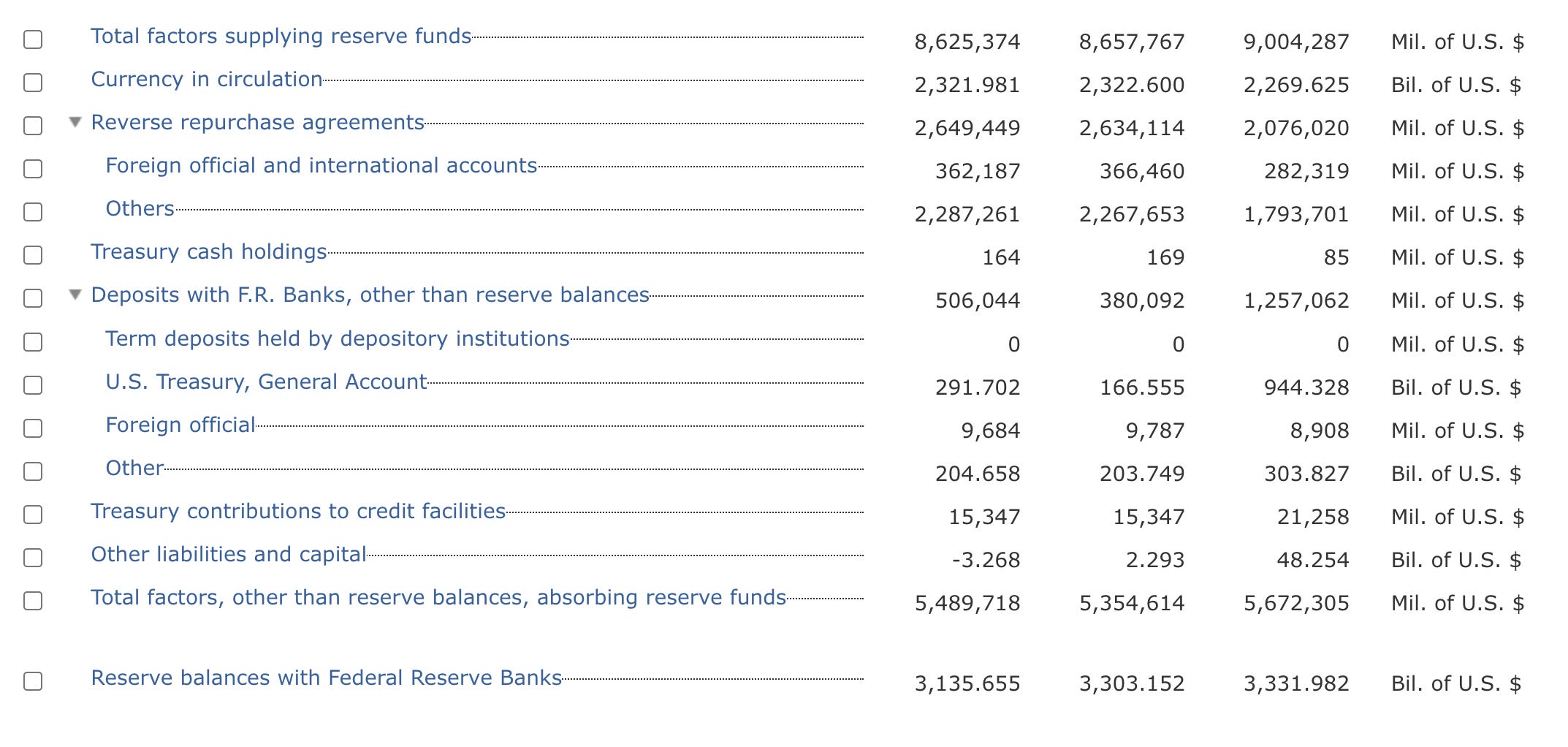

The link all the way at the bottom of the Factors Affecting Reserve Balances page on FRED, with title “Reserve Balances with Federal Reserve Banks” is WRESBAL. What makes this page useful is that WRESBAL can be calculated using the table, and by looking at the components that comprise the equation it can be better understood what influences this liquidity figure.

WRESBAL as of the end of April is a touch over $3 Trillion. The value can be calculated by taking “Total Factors Supplying Reserve” Funds (about $8.6 Trillion in this case), and subtracting each line below it, up until the “Other liabilities and capital” line. Let’s walk through this step by step:

First take Total Factors Supplying Reserve Funds: $8,625,374,000,000

Notice that this value is similar to WALCL, which is used in many liquidity equations to represent total assets, and WALCL can be found at the top of the FRED Consolidated Statement of Condition of All Federal Reserve Banks page by clicking the link titled “Total Assets”. Note: most of the US Fed signals that are available on TradingView are on this page, including WALCL.

Now subtract Currency In Circulation:

$8,625,374,000,000 - $2,321,981,000,000

= $6,303,393,000,000Subtract Reverse Repurchase Agreements (RRP):

$6,303,393,000,000 - $2,649,449,000,000

= $3,653,944,000,000Subtract Treasury Cash Holdings

$3,653,944,000,000 - $164,000,000

= $3,653,780,000,000Subtract Deposits with F.R. Banks, other than reserve balances (includes the Treasury General Account, also known as TGA)

$3,653,780,000,000 - $506,044,000,000

= $3,147,736,000,000Subtract Treasury contributions to credit facilities

$3,147,736,000,000 - $15,347,000,000

= $3,132,389,000,000Subtract Other Liabilities and Capital

$3,132,389,000,000 - (-3,268,000,000)

= $3,135,657,000,000And there is the final answer, WRESBAL! All of the subtracted components added together equal the “Total factors, other than reserve balances, absorbing reserve funds” line.

When expanding the categories in the factors absorbing reserve funds, we see something familiar in a lot of liquidity equations…

Notice the “U.S. Treasury, General Account” line, which is typically used in liquidity formulas with the ticker WTREGEN or WDTGAL. Both seem to be the same but WDTGAL is more recent data by one week, so I have updated my indicators on TradingView to use WDTGAL. Many of the simpler equations use WALCL - TGA - RRP, where TGA is Treasury General Account, and RRP is Reverse Repurchase Agreements. You can see in the table above, and the WRESBAL calculation that we used these variables, subtracted RRP, and TGA from the total factors supplying reserve funds, which is similar to WALCL - TGA - RRP.

You can see the similarities in these equations by charting both in the same view. In this case I’ll divide WRESBAL by a trillion to make the units the same (in trillions USD).

Notice that WRESBAL is at least a couple trillion dollars less than the WALCL - TGA - RRP equation. This indicates that WRESBAL includes more variables (factors absorbing reserve funds) as shown in the exercise above to calculate it with each line item. This further accuracy in what is available to markets in the form of liquidity is what gives WRESBAL its magic as the key ingredient to DEDO (Dark Energy Divergence Oscillator)

Using WRESBAL For Analysis/Indicators

WRESBAL is a great variable for tracking US Fed liquidity, and it often correlates well with asset price valuations, such as Bitcoin:

WRESBAL should not be confused with global liquidity, because it is only based on data that comes from the Federal Reserve balance sheet, so it is only factoring in US liquidity variables. For a deeper dive into my global liquidity equation, see my Central Bank Dark Energy Tracer (CBDET) article for details.

An advantage of using WRESBAL is that it’s a simple way to get a comprehensive value representing US central bank liquidity, including major factors such as the TGA, and RRP. On the downside it doesn’t let you pick apart the equation and provide optionality in terms of which components are used to track liquidity available to markets. This is why CBDET uses a different equation with individual components available in TradingView. By doing this CBDET is made more flexible, and can include/exclude variables via user settings.

I hope this article was helpful in explaining the WRESBAL variable on FRED. I intend to expand on this Fed series in the future, so please subscribe to get more great educational content in your inbox.